Inflation is here to stay

While governments cannot act on supply to mitigate inflation, they can affect demand by reducing liquidity by raising interest rates and taxes. Problem is that for the time being they can do neither.

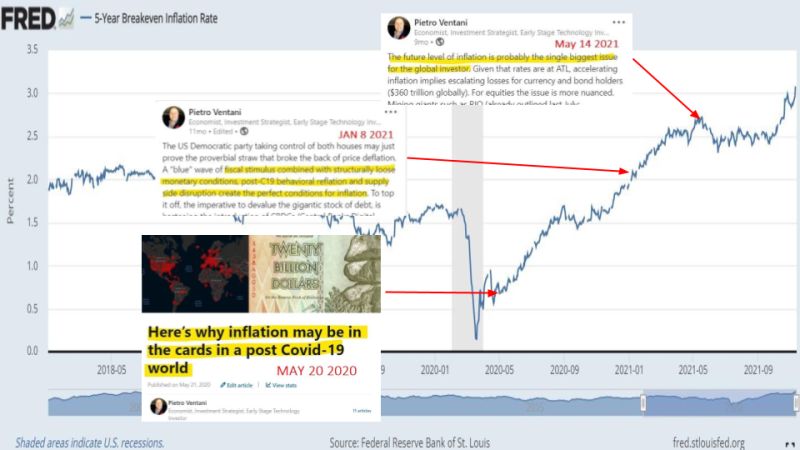

Last week’s inflation data shows that rising prices are here to stay. The writing was on the wall as opined frequently on these pages (see chart). On a very basic level, inflation is an unbalance between supply and demand. On the supply side the combination of pre-existing conditions and C19 has constrained supply of labor, energy, logistic capacity etc. On the demand side, unprecedented monetary and fiscal stimulus have generated massive incremental liquidity. The result has been too much money chasing too few goods and services. While governments cannot act on supply to mitigate inflation (you can’t “print” natural gas, truck drivers or food), they can affect demand by reducing liquidity by raising interest rates and taxes. Problem is that for the time being they can do neither. At least not in any meaningful way. Any tightening of financial conditions will tip the economy into recession and debase asset prices whose levels have been propped by ever low rates. Because of the enormous amount of leverage in the system, the former would trigger a domino effect of bankruptcies while the latter would then translate into the worst negative wealth effect since the 1930s. More importantly, policy makers know all too well that inflation is the only way to reduce debt through debasement. They are therefore keen to let it play out as much as possible. Behavioral economics is a powerful force and once the psychology of inflation is established, it becomes a self-fulfilling prophecy. Inflation is an equal opportunity scourge as it wreaks havoc on the life of both the more vulnerable strata of society and the savings of the more fortunate. It is, in a way, a transfer of wealth from the citizens to the state, whose debt is reduced in real terms. It is not a surprise that history shows that inflation is typically associated with increased political and geopolitical instability. The 2020s are going to be jarring and unfamiliar. Sovereign risks are mounting and portfolio strategies that have worked over the last three decades are of little use. Cognizant investors may want to start to re-think their approach. It is time to Swerve.