The 60/40 strategy is no longer viable

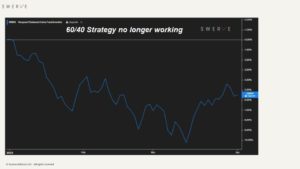

The 60/40 portfolio is one of the most widely used investment strategies is already down almost 6% YTD (see chart) and may no longer work. The principle of holding 60% of the portfolio in stocks and 40% in bonds is based on the belief that the two asset classes are inversely correlated, i.e. bonds would go up when equities decline and vice versa.

The 60/40 portfolio is one of the most widely used investment strategies is already down almost 6% YTD (see chart) and may no longer work. The principle of holding 60% of the portfolio in stocks and 40% in bonds is based on the belief that the two asset classes are inversely correlated, i.e. bonds would go up when equities decline and vice versa. The strategy worked as long as inflation was low, yields were trending down and the stock market trending up, a relationship that is no longer applicable in a stagflationary economy where both equities and bonds tend to fall because of persistent inflation and low growth. The prospect of stagflation was already apparent before the Ukraine war as opined on these pages over the last twelve months (https://lnkd.in/gSa9DsGW and https://lnkd.in/gvFc6RdR) The combination of a massive post C19 ”fiscal cliff”, obdurate inflation and the hesitancy of central banks to tighten monetary conditions because of debt, all pointed to such an outcome. While it is evident that historically elevated inflation is going to constrain real returns for fixed income, equities will also be challenged as indexes typically generate negative real returns during periods of slow growth and high inflation. The passive investing approach that worked so well for the last few decades is therefore not going to do as some sectors, e.g. commodities and real estate tend to outperform while, for example, industrials and technology do poorly. More importantly a careful assessment of sovereign risk and the consequent allocation to store of value assets, will play a key role in protecting wealth in the face of the political, geopolitical and social changes ahead. The majority of investors have never experienced stagflation and loss of capital in real and nominal terms is, from a basic accounting standpoint, inevitable and necessary to debase the massive stock of debt accumulated over the last decade. “The dogmas of the quiet past are inadequate to the stormy present” and it is time for investors to embark on a comprehensive rethink of portfolio strategies.