Energy is on a roll and yet investors seem to have hardly noticed

August 23, 2022 •

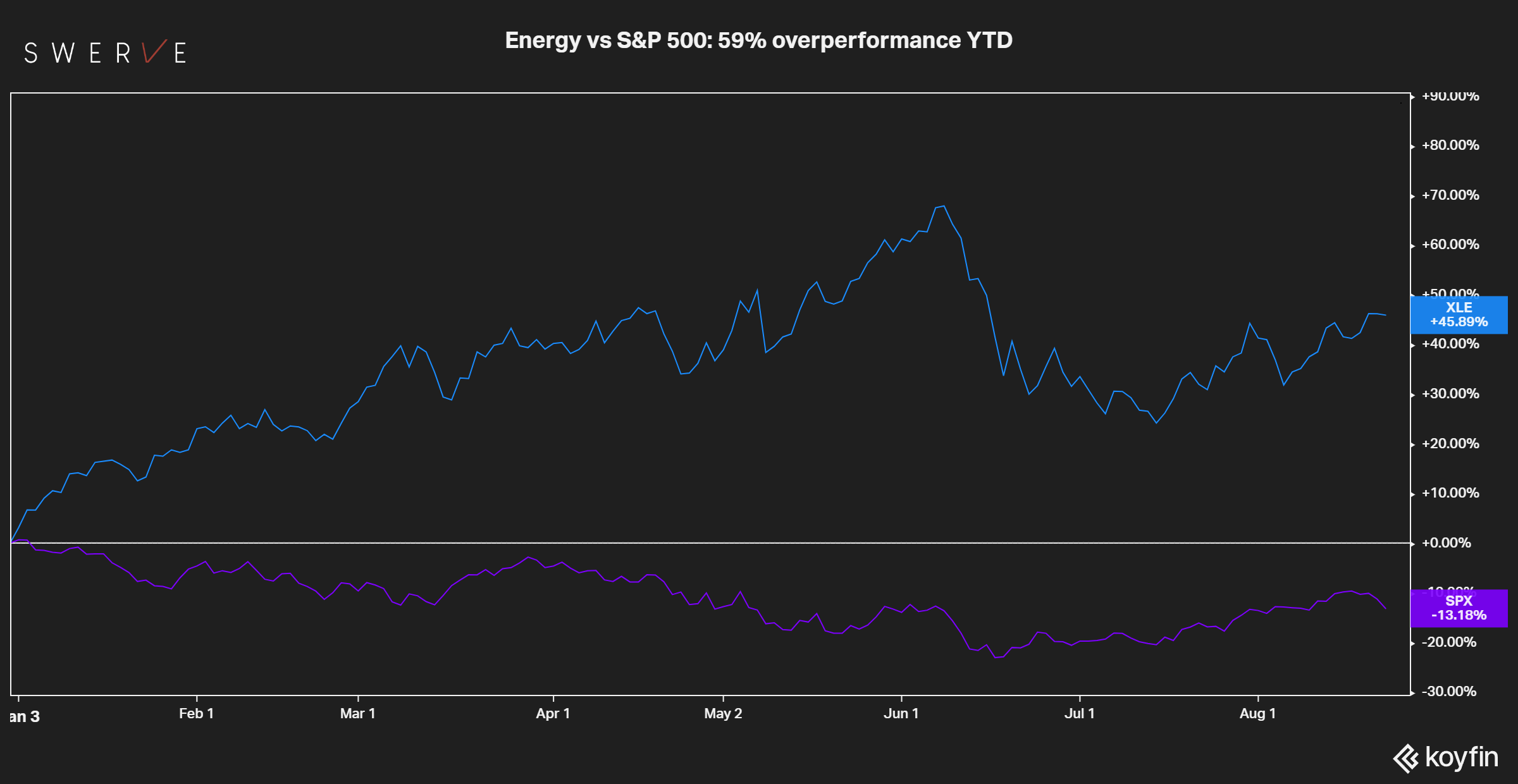

After four decades #energy is squarely back at the center of the economic, financial and political discourse. Yet investors seem to have hardly noticed. Even after a spectacular performance YTD, the energy sector is still a meager 4.2% of the total market capitalization and 40% below its 20 years average.

After four decades #energy is squarely back at the center of the economic, financial and political discourse. Yet investors seem to have hardly noticed. Even after a spectacular performance YTD (see chart comparison with the #S&P500) the energy sector is still a meager 4.2% of the total market capitalization and 40% below its 20 years average.

Moreover, even after the bull run, the forward PE for #Energystocks is 8.1 and the only still in the single digit among the 11 sectors. It appears that decades of #globalization hushed markets into believing that energy will always be cheap and available. A misplaced ESG narrative also contributed to the idea that energy investment is not only obsolete but, to a degree, politically incorrect. Especially when it comes to those companies that are still contiguous to the production and management of fossil fuel.

Those certainties have been thrown into question as we entered a new phase of #deglobalization (https://bit.ly/3QMzFDe). The last time that we saw disruption of the status quo akin to the present time was in the early 1970s. During that decade Energy’s S&P weight climbed from 7% in 1972 to 28% at year-end 1980. Granted the global economy has changed since and sectors such as Technology and Communications now represent the lion’s share of the economy. It is hard to imagine that Energy could again reach that 1980 level. Yet it is not unreasonable that energy companies’ valuations could double from the current very low levels.

As opined on these posts (https://bit.ly/3Av1k6D) a #stagflationary economy is likely to persist for some time. Data shows that during this type of economic regime energy is the best performing asset class and one of few generating a positive, inflation-adjusted return. As Machiavelli put it “Whoever wishes to foresee the future must consult the past”. Disclosure: Hold all assets mentioned. Not investment advice. Do your own research.