The great bond bull market has come to an end

November 21, 2022 •

While returns are unlikely to be stellar, in the current stagflationary conditions TIPs may be a reasonable alternative to cash and possibily deliver a positive return after inflation.

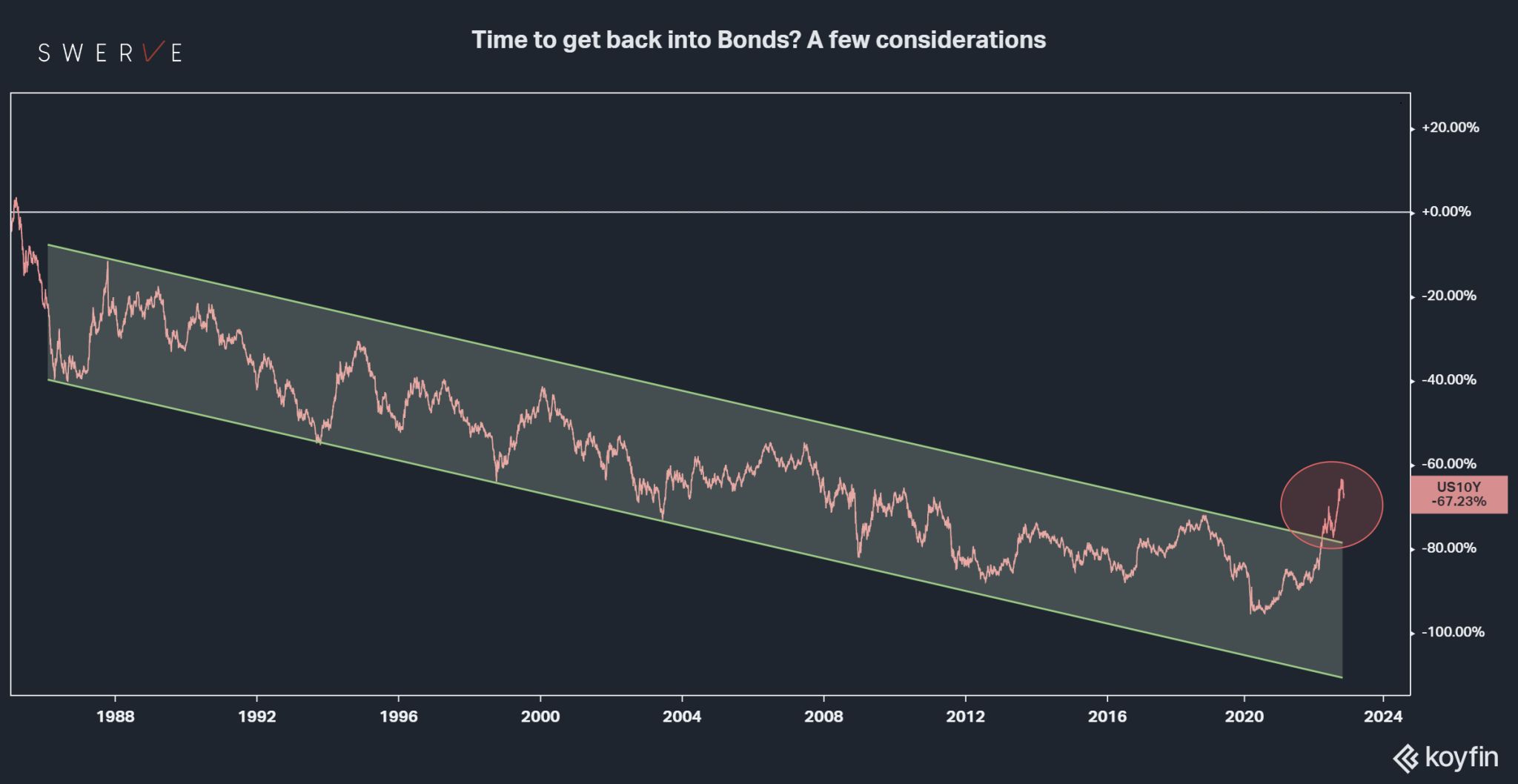

The great bull market started in 1986 has come to an end and #bonds had one of their worst years ever (see chart). As some investors are starting to wonder if it is time to get back into #fixedincome , a few considerations may help.

Rising interest rates have been responsible for the record negative performance for bonds this year and where we are in the tightening cycle is therefore a key element to consider. On this account, the good news is that the bulk of the rate hikes are behind with possibly another 150-200 bps in Fed Funds ahead that the market has largely factored in. The other key issue however is the reduction of the Fed’s balance sheet; should the Fed not roll over bonds in their portfolio, rates will continue to rise and weigh on prices. There is however significant probability that the Fed will not be able to meaningfully shrink their balance sheet and will rather choose to reduce it in real terms, rather than nominal, over the long term through yield curve control.

The level of inflation and economic growth are also a key consideration as these variables will largely determine monetary and fiscal policies. The four “Ds” of debt, deglobalization, demographics and decarbonization, all point to an inflationary bias, at least for the forseeable future. It is therefore likely we will not see the kind of aggressive rate cuts we became accustomed to since 2008 anytime soon as policymakers will need to keep rates higher to prevent an inflationary spiral.

As sustained price appreciation is unlikely to manifest at least for some time, the interest paid on the bond becomes the primary source of returns. Below-investment grade (“junk”) corporate bonds deliver the highest yield and possibly exceed inflation. Yet, the likely recession ahead, may increase the amount of non-performing loans and easily wipe off any returns. To this regard, European corporates look the most at risk as the economic outlook for the region is most uncertain.

All things considered, US government inflation-linked bonds, aka “TIPs”, may represent the better option for those investors wanting to get back into fixed income. In terms of principal, these bonds enjoy the security of the US government’s promise to repay, even though the Fed may need to “print” the money. As per the interest, the coupon is indexed to the official level of inflation and supposed to exceed it. While returns are unlikely to be stellar, in the current stagflationary conditions TIPs may be a reasonable alternative to cash and possibily deliver a positive return after inflation.

Disclosure: Hold all assets mentioned. Not investment advice. Do your own research. Twitter @pietroventani for more timely comments and updates.